您好,欢迎访问三七文档

当前位置:首页 > 商业/管理/HR > 经营企划 > 手把手教你织漂亮的贝雷帽 棒针帽子编织实例教程

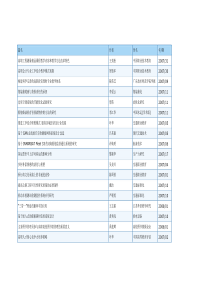

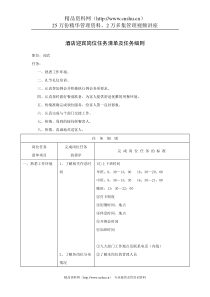

ChangestoPensionTaxReliefLimitsAnnualAllowancefrom6thApril2011LifeTimeAllowancefrom6thApril2012February2012workshopsUCLPensionServicesUCLPensionServices帽子–reducedlimitsToday’spresenters:FenellaNeedham–PensionsManagerUCL•AnnualAllowanceandLifeTimeAllowanceGaryO’Neill–AustinChapelIndependentFinancialAdvisers•Willyouneedfinancialadvice?InattendanceColleaguesfromUCLPensionServicesOverviewfortoday•WhatistheAnnualAllowance(AA)andLifeTimeAllowance(LTA)?•Whyhavetheychanged?•HowaretheAAandLTAcalculatedandwhatmightbethepotentialtaximplicationsforyou•ImpactofanyfuturepayincreaseorpaymentofanyfutureAVC’s•Actionsyouneedtoconsidergoingforward•ConsiderindependentfinancialadviceOutcomesfortoday•YouhaveagoodunderstandingoftheAAtaxchangesimplementedinApril2011–FinanceAct2011•Youareawareofthepotentialtaximpactcausedbyfuturepayincreases,continuedaccrualofpensionbenefitswhilstinany(butespeciallyafinalsalary)pensionschemeand/orpayingAVCs•Youknowwhen&fromwhomtogettherequiredinformationnecessaryforyoutocalculatetheAAandassesswhetheranytaxchargemaybedue•YouareawareofthepossibilityofapplyingforFixedProtectionbefore5thApril2012duetothereducedLTAlimit•YouknowwheretogetpensionsinformationandindependentfinancialadviceWhyhavetheAAandLTAchanged?•AAandLTAwerefirstintroducedApril2006–FinanceAct2004•AA(2006-preApril2011)was£255,000perannumandLTAwas£1.5min2006,risingto£1.8mfortaxyear2010/11•LimitssufficientlyhightonotaffectmanypeopleatUCL•FinanceAct2011madesignificantchangestotheregimeanditsoperation.•Labourgovernmentbroughtinchangesin2009whichaimedtobringanadditional£3.4Bnoftaxrevenue.Newgovernmentsimplifiedthemethodologybuthavesameincometarget.•From6April2011-AAreducedto£50,000•From6April2012–LTAreducedto£1,5mAnnualAllowance–whatisit?•Anannualthresholdorvaluebywhichyourpensionbenefitsmayincreasewithoutanypersonaltaxliability•AnyexcessovertheAAof£50,000paissubjecttotaxatyourmarginal(highest)rateoftax•AbilitytouseanyunusedAAfrompreviousthreetaxyearstooffsetanyexcessofAAinaPensionInputPeriod(PIP)previous3yearsusinganAAvalueof£50k•CarryForward-mechanismforprevious3yearsunusedallowanceAnnualAllowance–howisitcalculated?•PensionInputPeriod(PIP)-USSandNHSschemesboth1stAprilto31stMarch•CapitalValueofpension,lumpsum,AVCsatendofPIP•Factorof16(was10)•ConsumerPriceIndex(CPI)•Aimistoachieveadditionaltaxrevenuebymultiplemeans;•LowerlimitswillbringinmoreAAtaxcharges•EmployeeslimitingbenefitaccrualtonewAAlimitwillpayhigherPAYEthroughreducedtaxreliefonpensioncontributionsWhocouldbeaffected?-AnnualAllowance•Promotion(becomingDirector,Dean,ViceProvostorProvost!)andremaininginthesamepensionscheme•Annualprofessorial,clinicalandappraisalpayawards•PayawardsinexcessofCPI•Receivingaregradingorregradingamemberofyourstaff•Employingsomeone/movingjobswithinthesectorandremaininginsamepensionscheme•PayingAVCsorcontributionsintoanotherscheme•Accruingpensionatahigherratethanschemeaccrual,payingAddedYearsAVCs•Redundancy/Purchaseofadditionalservice(augmentation)byemployer•Combinationofhighsalary/longservice•Limitedscopetousepreviousunusedallowances•Note:DeferredbenefitsNOTincludedinAAcalculationsAnnualAllowance–Example1NoAVCspaid,nolargeincreaseinsalary•Earningsincreasefrom£100,000to£115,000on1stAugust2011•PIPpayfigurefor2011/12=((4/12x£100k)+(8/12x£115k))=£110,000•28yearsserviceat31/3/2011–29yearsserviceat31/3/2012•CPI(atSeptemberprior)=3.1%•Factorof16AnnualAllowance-Example1continuedTotalBenefitsforPIPto31/3/2011•28years/80x£100,000=£35,000+lumpsumof3xpension=£105,000•£35,000x16=£560,000+£105,000=£665,000•£665,000+3.1%CPI=£685,615TotalBenefitsforPIPto31/3/2012•29years/80x£110,000=£39,875+lumpsumof3xpension=£119,625•£39,875x16=£638,000+£119,625=£757,625AnnualAllowanceChargecalculation•£757,625-£685,615=£72,010•£72,675-£50,000=£22,010*40%=£8,804OffsetofpreviousyearsunusedAnnualAllowance–CarryForwardCalculations-toreduce/removeAAtaxliability–transitionalperiodYearAnnualAllowanceCarry-ForwardeachyearBalanceofCarry-Forward2010/11£30,000£20,000£40,0002009/10£60,000£nil£20,0002008/09£30,000£20,000£20,000TheabovecalculationmethodisusedforlookingbackoverthelastthreeyearsBalanceavailablecanbeusedtomitigate/removeachargeCalculationofunusedAnnualAllowance–CarryForwardCalculations-toreduce/removeAAtaxliability–goingforwardforfuturecalculationsYearAnnualAllowanceCarry-ForwardeachyearBalanceofCarry-Forward2010/11£30,000£20,000£30,0002009/10£60,000£nil£10,0002008/09£30,000£20,000£20,000TheabovecalculationmethodisusedforfuturecalculationsBalanceavailablecanbeusedtomitigate/removeachargeHowdoyoupaythetax,ifnoscopeleftafterCarryForwardcalculationsdone-“SchemePays”•YouwillneedtovoluntarilynotifyHMRCviaaSelfAssessmentTaxReturn(SATR)thatyouhaveexceededtheAA£50klimit.HMRCwillrequireyoutoimmediatelypayanyAACunder£2,000.•HMRCintroducedtheconceptof“SchemePays”-AAtaxchargeis£2,000+andisapplicableto1scheme,thenyoumayelectforthepensionschemetopaythechargeonyourbehalf.•YoumustinformHMRConyourSATRofyouroptionandinformyourpensionscheme

三七文档所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

三七文档所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

扫描二维码

扫描二维码

lefu168

lefu168

本文标题:手把手教你织漂亮的贝雷帽 棒针帽子编织实例教程

链接地址:https://www.777doc.com/doc-4026932 .html