您好,欢迎访问三七文档

当前位置:首页 > 商业/管理/HR > 管理学资料 > 跨国公司财务管理-Chap6

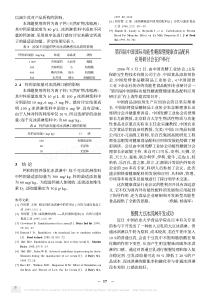

CHAPTER6MeasuringandManagingExposureToExchangeRateFluctuationsLiboYin,SchoolofFinance,CentralUniversityofFinanceandEconomicsEmail:yinlibowsxbb@126.comChapterObjectives1.MeasuringexposureTodiscusstherelevanceofanMNC’sexposuretoexchangeraterisk;Toexplainhowtransactionexposurecanbemeasured;Toexplainhoweconomicexposurecanbemeasured;andToexplainhowtranslationexposurecanbemeasured.2014/9/232CUFE--InternationalFinanceManagement2.ManagingtransactionexposureToidentifythecommonlyusedtechniquesforhedgingtransactionexposure;Toexplainhoweachtechniquecanbeusedtohedgefuturepayablesandreceivables;Tocomparetheadvantagesanddisadvantagesoftheidentifiedhedgingtechniques;andTosuggestothermethodsofreducingexchangerateriskwhenhedgingtechniquesarenotavailable.2014/9/233CUFE--InternationalFinanceManagement3.ManagingeconomicexposureandtranslationexposureToexplainhowanMNC’seconomicexposurecanbehedged;andToexplainhowanMNC’stranslationexposurecanbehedged.2014/9/234CUFE--InternationalFinanceManagementIsExchangeRateRiskRelevant?PurchasingPowerParityArgumentExchangeratemovementswillbematchedbypricemovements.PPPdoesnotnecessarilyhold.2014/9/235CUFE--InternationalFinanceManagementTheInvestorHedgeArgumentMNCshareholderscanhedgeagainstexchangeratefluctuationsontheirown.Theinvestorsmaynothavecompleteinformationoncorporateexposure.Theymaynothavethecapabilitiestocorrectlyinsulatetheirindividualexposuretoo.2014/9/236CUFE--InternationalFinanceManagementCurrencyDiversificationArgumentAnMNCthatiswelldiversifiedshouldnotbeaffectedbyexchangeratemovementsbecauseofoffsettingeffects.Thisisanaivepresumption.2014/9/237CUFE--InternationalFinanceManagementStakeholderDiversificationArgumentWelldiversifiedstakeholderswillbesomewhatinsulatedagainstlossesexperiencedbyanMNCduetoexchangeraterisk.MNCsmaybeaffectedinthesamewaybecauseofexchangeraterisk.2014/9/238CUFE--InternationalFinanceManagementResponsefromMNCsManyMNCshaveattemptedtostabilizetheirearningswithhedgingstrategies,whichconfirmstheviewthatexchangerateriskisrelevant.2014/9/239CUFE--InternationalFinanceManagementThefollowingcommentsfromrecentannualreportsofMNCsaretypical:Becausewemanufactureandsellproductsinanumberofcountriesthroughouttheworld,weareexposedtotheimpactonrevenueandexpensesofmovementsincurrencyexchangerates.—Procter&GambleCo.Increasedvolatilityinforeignexchangerates…mayhaveanadverseimpactonourbusinessresultsandfinancialcondition.—PepsiCo.2014/9/2310CUFE--InternationalFinanceManagementTypesofExposureAlthoughexchangeratescannotbeforecastedwithperfectaccuracy,firmscanatleastmeasuretheirexposuretoexchangeratefluctuations.Exposuretoexchangeratefluctuationscomesinthreeforms:TransactionexposureEconomicexposureTranslationexposure2014/9/2311CUFE--InternationalFinanceManagementTransactionexposureThedegreetowhichthevalueoffuturecashtransactionscanbeaffectedbyexchangeratefluctuationsisreferredtoastransactionexposure.Tomeasuretransactionexposure:projectthenetamountofinflowsoroutflowsineachforeigncurrency,anddeterminetheoverallriskofexposuretothosecurrencies.2014/9/2312CUFE--InternationalFinanceManagementTransactionexposureMNCscanusuallyanticipateforeigncashflowsforanupcomingshort-termperiodwithreasonableaccuracy.AftertheconsolidatednetcurrencyflowsfortheentireMNChasbeendetermined,eachnetflowisconvertedintoeitherapointestimateorarangeofachosencurrency,soastostandardizetheexposureassessmentforeachcurrency.2014/9/2313CUFE--InternationalFinanceManagementTransactionexposure2014/9/2314CUFE--InternationalFinanceManagementTransactionexposure2014/9/2315CUFE--InternationalFinanceManagementTransactionexposureAnMNC’soverallexposurecanbeassessedbyconsideringeachcurrencypositiontogetherwiththecurrency’svariabilityandthecorrelationsamongthecurrencies.2014/9/2316CUFE--InternationalFinanceManagementTransactionexposureThestandarddeviationstatisticonhistoricaldataservesasonemeasureofcurrencyvariability.Notethatcurrencyvariabilitylevelsmaychangeovertime.Thecorrelationsamongcurrencymovementscanbemeasuredbytheircorrelationcoefficients,whichindicatethedegreetowhichtwocurrenciesmoveinrelationtoeachother.coefficientperfectpositivecorrelation1.00nocorrelation0.00perfectnegativecorrelation-1.002014/9/2320CUFE--InternationalFinanceManagementTransactionexposure2014/9/2321CUFE--InternationalFinanceManagement£Can$¥NZ$SkSwFBritishpound(£)1.00Canadiandollar(Can$).181.00Japaneseyen(¥).45.061.00NewZealanddollar(NZ$).39.20.331.00Swedishkrona(Sk).62.16.46.331.00Swissfranc(SwF

三七文档所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

三七文档所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

扫描二维码

扫描二维码

sdoheji1234

sdoheji1234

本文标题:跨国公司财务管理-Chap6

链接地址:https://www.777doc.com/doc-578395 .html