您好,欢迎访问三七文档

当前位置:首页 > 行业资料 > 交通运输 > 事件研究法详解(event-study)

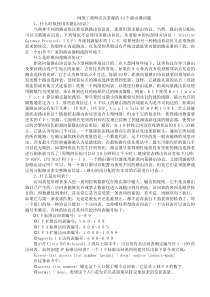

EventStudiesinFinancialEconomics:AReivewEventStudyAnalysis•Definition:Aneventstudyattemptstomeasurethevaluationeffectsofanevent,suchasamergerorearningsannouncement,byexaminingtheresponseofthestockpricearoundtheannouncementoftheevent.•Oneunderlyingassumptionisthatthemarketprocessesinformationabouttheeventinanefficientandunbiasedmanner.•Thus,weshouldbeabletoseetheeffectoftheeventonprices.0+t-tAnnouncementDateStockPriceEfficientreactionOverreactionUnderreactionPricesaroundAnnouncementDateunderEMH•Theeventthataffectsafirm'svaluationmaybe:1)withinthefirm'scontrol,suchastheeventoftheannouncementofastocksplit.2)outsidethefirm'scontrol,suchasamacroeconomicannouncementthatwillaffectthefirm'sfutureoperationsinsomeway.•Variouseventshavebeenexamined:–mergersandacquisitions–earningsannouncements–issuesofnewdebtandequity–announcementsofmacroeconomicvariables–IPO’s–dividendannouncements.–etc.•Techniquemainlyusedincorporate.•Simpleonthesurface,buttherearealotofissues.•Longhistoryinfinance:–Firstpaperthatappliesevent-studies,asweknowthemtoday:Fama,Fisher,Jensen,andRoll(1969)forstocksplits.–Today,wefindthousandsofpapersusingevent-studymethods.ClassicReferences•BrownandWarner(1980,1985):Short-termperformancestudies•LoughranandRitter(1995):Long-termperformancestudy.•BarberandLyon(1997)andLyon,BarberandTsai(1999):Long-termperformancestudies.•Eckbo,MasulisandNorli(2000)andMitchellandStafford(2000):Potentialproblemswiththeexistinglong-termperformancestudies.•Ahern(2008),WP:Sampleselectionandeventstudyestimation.•UpdatedReviews:M.J.Seiler(2004),PerformingFinancialStudies:AMethodologicalCookbook.Chapter13.KothariandWarner(2006),Econometricsofeventstudies,Chapter1inHandbookofCorporateFinance:EmpiricalCorporateFinance.EventStudyDesign•Thestepsforaneventstudyareasfollows:–EventDefinition–SelectionCriteria–NormalandAbnormalReturnMeasurement–EstimationProcedure–TestingProcedure–EmpiricalResults–InterpretationTime-line•Thetime-lineforatypicaleventstudyisshownbelowineventtime:-TheintervalT0-T1istheestimationperiod-TheintervalT1-T2istheeventwindow-Time0istheeventdateincalendartime-TheintervalT2-T3isthepost-eventwindow-Thereisoftenagapbetweentheestimationandeventperiods•IssueswiththeTime-line:-Defintionofanevent:Wehavetodefinewhataneventis.Itmustbeunexpected.Also,wemustknowtheexactdateoftheevent.Datingisalwaysaproblem(WSJisnotagoodsource-leakage).-Frequencyoftheeventstudy:Wehavetodecidehowfasttheinformationisincorporatedintoprices.Wecannotlookatyearlyreturns.Wecan’tlookat10-secondsreturns.Peopleusuallylookatdaily,weeklyormonthlyreturns.-SampleSelection:Wehavetodecidewhatistheuniverseofcompaniesinthesample.-Horizonoftheeventstudy:Ifmarketsareefficient,weshouldconsidershorthorizons–i.e.,afewdays.However,peoplehavelookedatlong-horizons.Eventstudiescanbecategorizedbyhorizon:-Shorthorizon(from1-monthbeforeto1-monthaftertheevent)-Longhorizon(upto5yearsaftertheevent).Shortandlonghorizonstudieshavedifferentgoals:–Shorthorizonstudies:howfastinformationgetsintoprices.–Longhorizonstudies:Argumentforinefficiencyorfordifferentexpectedreturns(oraconfusingcombinationofboth)Modelsformeasuringnormalperformance•Wecanalwaysdecomposeareturnas:Ri;t=E[Ri;t|Xt]+ξi,t,whereXtistheconditioninginformationattimet:•Ineventstudies,ξi;tiscalledthe“abnormal”return.•Q:Whyabnormal?Itisassumedthattheunexplainedpartisduetosome“abnormal”eventthatisnotcapturedbythemodel.•Inasense,wewanttogetclosetoanaturalexperiment.–Thereisanexogenous(unanticipated)shockthataffectssomestocks.–Wewanttocomparethereturnsofthosestocksaroundtheannouncementtoothersthatarenotaffected.•Definitionof“Normal”Returns:Weneedabenchmark(controlgroup)againstwhichtojudgetheimpactofreturns.–Thereisahugeliteratureonthistopic.–FromtheCAPM/APTliterature,weknowthatwhatdrivesexpectedstockreturnsisnotexactlyclear.–Thisispreciselywhatweneedtodoineventstudies:Weneedtospecifyexpectedreturns(wejustcallthem“normal”returns).–Notethatifwearelookingatshorthorizonstudies,wecanassumethatexpectedreturnsdonotchange.Noproblem,here.–Ifwearelookingatlonghorizons,weknowthatexpectedreturnschange.Bigproblem.Wehavetobecareful.–Inlonghorizonstudies,thespecificationofexpectedreturnsmakesahugedifference,becausesmallerrorsarecumulated.Thereisnoeasywayoutofthisproblem.Statisticaloreconomicmodelsfornormalreturns?•Statisticalmodelsofreturnsarederivedpurelyfromstatisticalassumptionsaboutthebehaviorofreturns-i.e.,multivariatenormality.-Multivariatenormalityproducestwopopularmodels:1)constantmeanreturnmodeland2)themarketmodel.Note:Ifnormalityisincorrect,westillhavealeastsquaredinterpretationfortheestimates.Actually,weonlyneedtoassumestabledistributions.SeeOwenandRabinovitch(1983).•Economicmodelsapplyrestrictionstoastatisticalmodelthatresultfromassumedbehaviormotivatedbytheory-i.e.,CAPM,APT.–Iftherestrictionsaretrue,wecancalculatemoreprecisemeasuresofabnormalreturns.–CLM:“thereseemstobenogoodreasontouseaneconomicmodel.”PopularStatisticalModelsConstantmeanreturnmodel•Foreachasseti,theconstantmeanreturnmodelassumesthatassetreturnsaregivenby:Ri,t=E[

三七文档所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

三七文档所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

扫描二维码

扫描二维码

canxing110

canxing110

本文标题:事件研究法详解(event-study)

链接地址:https://www.777doc.com/doc-6361097 .html