您好,欢迎访问三七文档

当前位置:首页 > 商业/管理/HR > 经营企划 > derivatives加拿大著名咨询公司在建设银行的讲座5

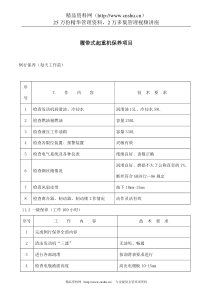

DerivativesLecture#5Derivatives2DerivativesDefinition:Aderivativesecurityisasecuritywhosemarketvalueisdeterminedbythevalueofanother,underlyingsecurityFunctionshedgingspeculationRisksinabilitytounderstandinabilitytoformaperfecthedgecostDerivatives3DerivativeInstrumentsMarketsTradedorlistedmarketsOTCHedgingInstrumentsInsuranceInstrumentsDerivatives4HedgingInstrumentsForwardcontractsAcontractagreedupontotodaytodeliveraspecifiedgoodataspecifiedpriceataspecifiedfuturedateFuturescontractsAstandardized,exchange-tradedforwardcontractForwardRateAgreementsTakeaviewastofutureinterestratesSwapsAnexchangeofinterestand/orcurrencyflowsDerivatives5InsuranceContractsOptionContractsTheright,butnottheobligation,toeitherbuy(calloption)orsell(putoption)somethingataspecifiedpriceforaspecifiedperiodoftime.Floors,capsandcollarsMethodsofchangingtheinterestrateriskofafloatingratedebtobligationSwaptionsAnoptiontoenterintoaswapataspecifiedfuturedateDerivatives6ForwardContractsMarketPriceDeliveryPrice+-0PayoffDiagram:LongtheForwardYoutakedeliverywhenlongtheforward.Thelongforwardpositionwillbenefitwhenmarketpricesriseafterthecontractisinitiated.Derivatives7ForwardContractsMarketPriceDeliveryPrice+-0PayoffDiagram:ShorttheForwardYoumakedeliverywhenshorttheforward.Theshortforwardpositionwillbenefitwhenmarketpricesfallafterthecontractisinitiated.Derivatives8ForwardMarkets&InterestRatesThemostliquidforwardmarketisthe“when-issued”TreasuryBillmarket.Dealersandinvestorsbuyandselltheas-yet-unissuedTreasuryBillfordeliveryimmediatelyaftertheyareissuedatauction.Theactivityinthe“when-issued”marketisagoodindicatorofwherethemarketbelievesratesareheadedDerivatives9HedgingInterestRateswithForwardContractsSupposeyouareholding$1,000,000insixyear,8%couponEurobondscurrentlytradingatpar.Youbelievethatinterestrateswillsoonriseby2%.Howdoyouhedgetheportfolio?Step#1:Calculatethebond’sdurationDuration=4.99271Step#2:PredictcapitallossP=(-D)(P)(R/1+R)=-$92,457Step#3:Adjustforconvexity(orcalculateactualpriceatnewmarketinterestrateof10%)Price=$912,894.79Actuallossthusequalto$1,000,000-912,894.79=$87,105.21Derivatives10HedgingInterestRateswithForwardContractsStep#4:HedgeSellthebondforwardforsaleinsixmonthsatapriceof$100per$100offacevalue.Ifinterestratesriseaspredicted,purchasethebondinthemarketfor$912,894.79anddeliverundertheforwardcontract.Collect$1,000,000.Profitontheforwardexactlyoffsetsthelossonthebondportfolio.Ifratesfallinsteadofrise,youwillincuraloss,asyouwillhavetodeliverthebondatapricebelowitsmarketprice.Derivatives11ComparingFutures&ForwardsForwardFutureStandardizedNoYesExchange-tradedNoYesMarked-to-marketNoYesProfits&lossessettleddailyNoYesMarginrequiredNoYesExistenceofclearinghouseNoYesDerivatives12ForwardRateAgreementsAssumethat,asabankmanager,youarefacingthefollowingsituation:Sixmonthinterestratesare10.5%.Threemonthinterestratesare10%.Whatthreemonthinterestrate,threemonthsfromtoday,wouldmakeusindifferentbetweeninvestinginonesixmonthinstrumentortwo,threemonthinstruments?Howcouldthebankprofitfromthisinformation?Derivatives13ForwardRateAgreements10.5%10%X%ThreemonthsThreemonthsSixMonthsDerivatives14ForwardRateAgreementsTosolvetheproblem,wemustsolvethefollowingequationfortheforwardinterestrate,rfwd/fwd:LongShortfwd/fwdLongfwd/fwdShortrrrDDDBBBrDBBrrDDB111100100100110011001100Derivatives15ForwardRateAgreementsWhere:D-numberofdaysintheperiodB-AnnualbasisrLong-ThespotsixmonthinterestraterShort-Thespotthreemonthinterestraterfwd/fwd-ThethreemonthforwardinterestrateDerivatives16ForwardRateAgreementsfwd/fwdfwd/fwdr..r.%105181109190111100360100360100360105181136010036011001091901100360107342Solvingtheproblem,weobtainthefollowingsolution:Derivatives17ForwardRateAgreementsAtayieldof10.7342%onthreemonthmoneythreemonthsfromtoday,youwouldbeindifferentbetweeninvestinginonesixmonthinstrumentortwo,threemonthinstruments.Howcouldthebankmanagerprofitfromthisinformation?Ifthebankisabletoobtaintwo,threemonthdepositsatarateof10%andthenlendthemoneyat10.5%,thebankisassuredofmakingaprofitbasedonthemismatchinterm.Derivatives18ForwardRateAgreementsBankschangetheirGAPwhentheyborrowandlendwithdifferentmaturities.NegativeGAPoccurswhenthebankborrowsshorttermandlendslongterm.Theriskisthatshortinterestrateswillrisebeforethelongassetmatures.Howwouldwecalculatetheprofitthebankwouldmakeifitcouldborrow$100,000,000at10%fortwo,threemonthperiodsandinvestthefundsat10.5%forsixmonths?Derivatives19ForwardRateAgreementsTosolvetheproblem,usethefollowingformula:BreakevenActualrrDProfitPrincipalB..,,$,100107342100090100000000360100183550Derivatives20ForwardRateAgreementsProblemswithusingforward/forwardsCreditrisk-thebankincurscreditriskonthelendingtransactionCapitalcharges-thebankmustholdadditionalcapitalagainstitslargerbalancesheetLinesofcredit-thebankisusingupitscreditcapacitywiththeborrowingtrans

三七文档所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

三七文档所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

扫描二维码

扫描二维码

我是文丑

我是文丑

本文标题:derivatives加拿大著名咨询公司在建设银行的讲座5

链接地址:https://www.777doc.com/doc-694492 .html