您好,欢迎访问三七文档

当前位置:首页 > 商业/管理/HR > 项目/工程管理 > 面向优质建设与房地产开发的专业化进程

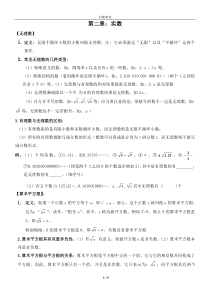

AtransactionbasedapproachforassessingtheriskandreturnofpropertyinvestmentinHongKong产数评产资风险报ProfessionalismtowardsQualityConstructionandPropertyDevelopment质设产开发专业进设产热点问题讨会资单别区办单测师学会济学学协办单华络学华学学国学济学创Residentialsub-sector050100150200250300350400450198019811982198319841985198619871988198919901991199219931994199519961997199819992000200120022003Index(1989=100)PriceRentRetailsub-sector050100150200250300350400450198019811982198319841985198619871988198919901991199219931994199519961997199819992000200120022003Index(1989=100)PriceRentOfficesub-sector050100150200250300350400450198019811982198319841985198619871988198919901991199219931994199519961997199819992000200120022003Index(1989=100)PriceRentIndustrialsub-sector050100150200250300350400450198019811982198319841985198619871988198919901991199219931994199519961997199819992000200120022003Index(1989=100)PriceRent9797//-6%-18%-8%-14%Averagetotalannualreturnh73%-59%-59%-65%1997Q3-2003Q215%17%21%21%Averagetotalannualreturn253%512%907%862%1983Q3-1997Q2IndustrialOfficeRetailResidential9797//(())-2%-14%-5%-10%Averagetotalannualreturnh-49%-66%-49%-56%1997Q3-2003Q28%10%13%13%Averagetotalannualreturn33%131%280%263%1983Q3-1997Q2IndustrialOfficeRetailResidential(1980:Q1(1980:Q1--2003:Q2)2003:Q2)19.0%13.5%9.3%11.2%Risk()7.0%11.1%9.2%10.5%AveragetotalReturn19.5%13.8%10.0%10.9%Risk()1.8%5.6%1.7%5.4%Averagereturn()IndustrialOfficeRetailResidential(())(1980:Q1(1980:Q1--2003:Q2)2003:Q2)20.5%15.0%10.8%12.7%Risk()2.4%6.5%4.6%5.9%AveragetotalReturn21.0%15.3%11.5%12.4%Risk()-2.8%1.0%-3.0%0.8%Averagereturn()IndustrialOfficeRetailResidentialRReealEstatePriceasaneconomicindicatoralEstatePriceasaneconomicindicatorLeadseconomicgrowth(GDP)Leadseconomicgrowth(GDP)Byapproximately2Byapproximately2qtrsqtrsinHongKonginHongKongLeadsrealestateinvestmentLeadsrealestateinvestmentLeadingIndicatorsLeadingIndicators(())PropertysharepricesPropertyshareprices(())TransactionVolumeTransactionVolume(())PrePre--salespricessalesprices(())RealandnominaldiscountratesRealandnominaldiscountratesNominaldiscountformulaNominaldiscountformulawheregisexpectedfuturegrowthrateinrent(wheregisexpectedfuturegrowthrateinrent())Aiscurrentrentalincome(Aiscurrentrentalincome())RRNNisnominaldiscountrate(isnominaldiscountrate())RealdiscountformulaRealdiscountformulaRisrentalyield(Risrentalyield())V=A(1+g)(1+RtNtt=1n)∑VA(1)tt1n=+=∑RImpliedexpectedlongtermrentalgrowthImpliedexpectedlongtermrentalgrowth(())Comparingthetwoformula(Comparingthetwoformula())RRNN=R+g+=R+g+RgRgRRNNThenominaldiscountratehastwocomponents(Thenominaldiscountratehastwocomponents())RRNN=R=RFF+R+RPPRRFFRRPPR=RR=RFF+R+RPP––gg––RgRgg=Rg=RFF+R+RPP––RRLeadingIndicatorsLeadingIndicators(())DifferencebetweenimpliedexpectedlongDifferencebetweenimpliedexpectedlong--termrentalgrowthandexpectedlongtermrentalgrowthandexpectedlong--termterminflationinflation(())LI=gLI=g--EE(Inf(Inf))whereEwhereE(inf(inf)isexpectedlong)isexpectedlong--terminflationterminflationEE(inf(inf))LongtermrentalgrowthandInflationLongtermrentalgrowthandInflationInthelongrunrentalgrowthshouldbeInthelongrunrentalgrowthshouldbesimilartoinflationsimilartoinflationIfattimet,Ifattimet,ggttEE(inf(inftt),i.e.(LI0)thenreal),i.e.(LI0)thenrealestatepriceislikelytobeovervaluedandestatepriceislikelytobeovervaluedandwillbecorrectedintheFUTUREwillbecorrectedintheFUTURELI0LI0EstimationofLeadingIndictorLIEstimationofLeadingIndictorLIImpliedlongImpliedlong--termexpectedrentalgrowthisestimatedtermexpectedrentalgrowthisestimatedusingusingg=Rg=RFF+R+RPP––RRRRFFistakenaslongtermgovernmentBondYield(30yearsistakenaslongtermgovernmentBondYield(30years+Premium)+Premium)RRFFRpRpistaketobeconstant(2%)istaketobeconstant(2%)RpRp=2%=2%RisestimatedfromdataobtainedfromRatingandRisestimatedfromdataobtainedfromRatingandValuationDepartmentValuationDepartmentEstimationofLeadingIndictorLIEstimationofLeadingIndictorLIExpectedLongterminflationrateisestimatedExpectedLongterminflationrateisestimatedfrompreviousinflationsratesfrompreviousinflationsratesInthisstudy,itistakenas5yearmovingaverageInthisstudy,itistakenas5yearmovingaverageofquarterlychangesinGDPdeflatorofquarterlychangesinGDPdeflator55ResidentialSub-sector-10%-8%-6%-4%-2%0%2%4%6%8%1978197919801981198219831984198519861987198819891990199119921993199419951996199719981999200020012002TimeExp(Pricegrowth)-Exp(Inflation)3.03.54.04.55.05.56.06.5Ln(ResidentialPriceIndex)LI(Res)Ln(RPI_Nominal)L(res)=1.6%in1981:Q1Pirceindexpeakedin1981:Q3Pirceindexfellby32%formthepreviouspeakin1983:Q3Pirceindexpeakedin1997:Q3Pirceindexfellby61%formthepreviouspeakin2002:Q4L(res)=0.9%in1997:Q1ResidentialSub-sector(Quarterlyreturn)-10%-8%-6%-4%-2%0%2%4%6%8%1978197919801981198219831984198519861987198819891990199119921993199419951996199719981999200020012002TimeExp(Pricegrowth)-Exp(Inflation)-25%-20%-15%-10%-5%0%5%10%15%20%25%NominalreturnLI(Res)NominalReturnRES_NRt=C+βRES_Lit-1+RES_NRt-1+εDependentVariable:RES_NRMethod:LeastSquaresDate:12/02/03Time:03:23Sample(adjusted):1978:3

三七文档所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

三七文档所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

扫描二维码

扫描二维码

6883252

6883252

本文标题:面向优质建设与房地产开发的专业化进程

链接地址:https://www.777doc.com/doc-95389 .html