您好,欢迎访问三七文档

当前位置:首页 > 商业/管理/HR > 企业财务 > 自由现金流的股利分配

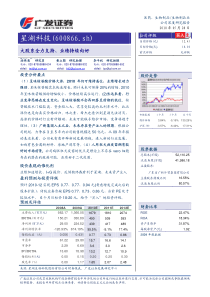

10011TITLETheResearchaboutDividendBasedonFreeCashFlow200506205020013200450%iAbstractDividendpolicyoflistedcompanyisakeypartinmaximizingcompanyvalue,anditisalsoanimportantwayforinvestortoobtaininvestmentrepayment.Asapartofcorporationfinancialpolicy,theissueofdividendpolicyhaslongbeenstudyinginwesternfromthe1950's.Westernscholarshaveconductedalotoftheoreticalstudiesandempiricalanalysesandputforwardvarioustheorieswithdifferentideasfordividendpolicy.Incomparisonwiththeoverseasresearch,wehavenotpaidmoreattentiontothetheoreticalandempiricalstudiesofdividendpolicy,thestudyofthepolicyhasjustbeguninChinaandstillbeenatthestageofneglect.Justbecausewehavenothedividendtheoryandexperience,Atpresent,thedeterminantsofdividendpolicyoflistedcompanyisstilluncertain,Theirregulardividendpolicyhasnotmerelydamagedtheinterestsofmediumandsmallinvestors,twistedtheinvestmenttheoryofthemarket,butalsoimpairedcompanyvalueprotectthetradableshareholdersthegovernancerelatedthedividendpolicywithnewfinancingin2001and2004.Thenmostofcorporationsbegantopaydividends.Andatthesametime,policyhasshowedmorenonstandardcharacters,suchasexcessdividendlowdividendlargecashdividendwithdrewbynontradableshareholderswhocandeterminedividendpolicy.Thispaperdisclosestheproblemsofcashdividendoflistedcompanyinrecentyears,analyststhecauseofthem,andofferssomeideastosolvethem.Thepaperisdividedintofourchapters.InChapter1,thispaperreviewsagreatdealofrelevantliteratureinwesterncountryandChina,andtheresearchbackgrounds,researchcontent,researchmethods,andthestructureofthisarticlearebrieflyintroduced.InChapter2thepaperanalyststhreemodelsofdividendscashdividendandputforwardfreecashflowthatthecashdividendisfrom.InChapter3,thethesisanalyzesthecharactersandtheproblemsofcompanies'cashdividendinChina.MeanwhilethemainreasonsaccordingtotheactualsituationinChinaarethegovernmentforcingdividendpolicyandtheneglectoffreecashflow.Basedonthis,thelastchaptersuggestssomemeasurestosolvetheproblemsofcashdividendoflistedcompaniesKeywordslistedcompaniesdividendpolicyresidualdividendpolicyiifreecashflow...............................................................11.1..........................................................11.2.......................................................21.3.............................................................21.4...................................................5..............................................62.1...................................................62.2.......................................72.3.......................................................82.4FCF............................................9..................................163.1............................................163.2....................................193.3................................22............................264.1................................264.2..............................284.3...........................................................294.4.............33.......................................................................35...................................................................36...........................................................38.......................................................................39iii1.12000(/):1999200020012002200359.5%,53%49%56%43%2000(0.380.66)(0.30.3)11.2901.3111Jensen,Meckling(1976)Easterbrook(1984)JensenMeckling2(1976)2(freecashflow)Easterbrook(1984):2(signalinghypothesis)22000()(2001)3:20022000-20012000(ROE)[6%,7%](2002)1997-2000(/)20032000299()(2000);41.45(dividendpolicy)()2.112345662.212732.31BarkerFarrelyEdelman1983373%75%2832.4FCF:,:,,,,,,,9,,,,,,,,,,,,,,,,,:12103456(1989)111986(BradfordCornell)1993FinEconK.S.Hackel1996SystematicFinancialManagement,L.P.discretionaryTomCopeland(1990)McKinsey&Company,Inc.NetOperatingProfitlessAdjustedTax,NOPAT1122345TomCopeland=+-+,,,,214,()=(EBITDA)=+,:==(EBITDA)+()(EBIT),,,132121:(),,,,,,14,,,,,,,Jensen(1986):JensenJensenJensen153.13-13-1,3-211994-199521995-1996199531996-19971996310%10%41997-199919989851999-20011999200116200162001-2003200120041272004200437182004497200469%573.97182.2031.74%54.33%17311994-20035199428319769.61199530724780.46199651020940.98199771539354.97199882127133.00199991832435.292000105464361.012001113068860.882002119361851.802003125261148.800200400600800100012001400199419951996199719981999200020012002200331180102030405060708090199419951996199719981999200020012002200332199420033.2120022003103()2004-0.34482004106()121.5%2003107106.9%200210599.81%2001101.2830.47%20012002200360.72%20031922?32004718522005323151180052450%200482783.77104.2()2.82171.43%23(0.05)2002200165.21%20023-2100.519931994199519961997199819992000200120020.518112320262834128111621832.91323530745851938108811601224%9.843.787.123.773.493.293.6211.769.575.073200449717%2020%120.110234(600588)20012001106()600055.2%3321(600588)0.6()33218000450054%2015001.6%13360001332136.68IPO1.6%64213.312001200420013200412732002200420030.03(000897)10220.30582,(),,,,,,(),,,(cashisking),,(freecashflowtoequity,FCF

三七文档所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

三七文档所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

扫描二维码

扫描二维码

starms

starms

本文标题:自由现金流的股利分配

链接地址:https://www.777doc.com/doc-1214105 .html