您好,欢迎访问三七文档

当前位置:首页 > 商业/管理/HR > 创业/孵化 > 中国股市IPO高抑价现象研究

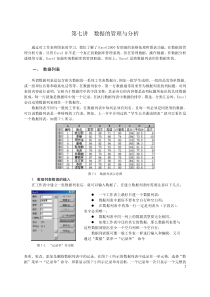

1TheStudyofHighIPOUnderpricinginChina’sStockMarket2IPO20019200473IPOIPOIPOIPOIPOIPO60IPOIPOIPOIPOIPOIPOIPOIPO4IPOIPO100%IPOIPO1234IPOEVAIPOIPOSignalModelWinnersCurseInformationalCascade5RitterIPOIPOIPOIPOIPOIPOIPOIPOIPOIPO1IPO26IPOIPOIPOIPOIPOAbstractAlargenumberofresearcheshaveshownthatInitialpublicofferingunderpricinguniversallyexistsinalmosteverycountryoftheworld,notonlyinthedevelopedcountriesbutthedevelopingones.ButthedegreesofIPOunderpricingaredifferent.Comparedwithotherstockmarket,theIPOunderpricinginChina’sstockmarketisobviouslyseverehigh.ThehighunderpricinginfluencesChina’sstockmarket,whichevenmakesagainstthehealthyofthewholeeconomic.Therefore,thestudyofIPOunderpricinginChina’sstockmarketismeaningfullyimportantbothinpracticeandintheory.ThetheoreticalandempiricalresearchonIPOunderpricingisahotanddifficultissuewhichattractsacademicsverymuch.TheacademicsofothercountriespayattentiontoIPOunderpricingin1960’s.Ontheconditionofmaturemarket,basedondifferenttheories,theyofferedalotofexplanationsforunderpricing.WiththedevelopmentofChina’sstockmarket,ChineseacademicshavedonemanyempiricalanalysisworksonChina’sIPOunderpricing.BecauseChina’sstockmarketisinaspecialdevelopingstage,therearemanydifferencesfrommutualcountries.Besides,China’sstockmarkethasbeeninreformprocess,theconditionofresearchisdifferent.So,tofindoutthetruereasonofhighIPOunderpricinginChinawillbenefittothereformofChina’sstockmarket.WewillstudythehighIPOunderpricinginChina’sstockmarkettofindtheessentialreasoninourarticle.ThenwecanunderstandthepriceruleofChina’sstockmarketandgivesomesuggeststothereform.Theremainderofthisarticleisorganizedasfollows.InSectionI,weanalyzethecharacteristicofIPOunderpricinginChina’sstockmarket.Firstly,IPOunderpricingisasystematicincreasefromtheofferpricetothefirstdayclosingprice.Academicsusethetermsfirst-dayreturnandunderpricinginterchangeably.ThedegreeofIPOunderpricingismeasuredbythefirst-dayreturn.Secondly,accordingtothecontrastofIPOunderpricingsindifferentstockmarkets,wefindoutthatthefirst-dayreturninChina’sstockmarketisseverehighinrecentyear.Thirdly,IPOunderpricingbringsdisadvantageousinfluence.(1)TherearealargeamountofmoneyinIPOmarket,andlackofmoneyinexchangemarket.(2)TherearenoriskinIPOmarketandhighriskinexchangemarket.(3)IPOunderpricingenlargestheriskanddistortsthepriceintheexchangemarket.(4)IPOunderpricinginducesunderwriterstocompeteoutoforder.Becauseoftheabovereasons,governmentpublishedmanypolicestoadjustandreformtheIPOsystem.Buttherearestillalotofproblems.Finally,weputforwardhowtofindtherealreasonofseriouslyhighIPOunderpricinginChina’sstockmarket.China’sstockmarketisnotanefficientmarket,sowecan’tdirectlyuseothercountry’stheoriestoexplainthehighIPOunderpricinginChina.Wewillexplaintheissuebasedonthebehaviorfinancetheoryandexchangeinteresttheory.Wewillanalyzethebehaviorandmindofthe4partsinIPOactivities.SectionIIintroducesthemodelandtheoryofIPOpricing.Therearetwopartsinthissection.First,theestimatemodelsofcompany’svalueincludediscountedcashflowapproach,marketapproachandEVAapproach.Then,weintroducedBookbuilding,FixedPriceIPO,TenderorAuctionIPOandHybridIPO.Basedonthetheories,wediscussedtheIPOpracticeinChina’sstockmarket.Theyarethefoundationofthefollowinganalysis.SectionIIIcoverssometypicaltheoriesofIPOunderpricinginwestcountries.Weclassifytheexplanationsinto3parts.TheTheoriesbasedonAsymmetricInformationincludeSignalModel,Winner’sCurse,InformationalCascadeandasymmetricinformationexplanationinbookbuilding.BasedonSymmetricInformation,onewayofinterpretingIPOunderpricingisthatissuersunderpricetoreducetheirlegalliability,theotherwayisthatunderwriterswere“leaningagainstthewind”bynottakingadvantageoftemporaryoveroprimismonthepartofsomeinvestors.Butthesetheoriesareunlikelytobetheprimarydeterminationfluctuations,especiallytheexcessesoftheinternetbubbleperiod.Instead,academicsbelievedspecialnon-rationalexplanationsandagencyexplanationswillplayabiggerroleinthefutureresearchagenda.Indiscussingtheoriesofunderpricing,theydevotesignificantattentiontothetopicofshareallocationsandsubsequentownership.WeintroducedtheIntermediary’sReputationHypothesis,Ritter’sConflictTheoryofInterestandPriceStabilizationTheory.Therearemanyempiricalpaperstoexamallthesetheories.SectionIVpresentsevidenceandanalysisofChina’shighIPOunderpricing.Firstly,ourarticlereviewstheChineseacademics’researchresultsonhighIPOunderpricinginChina.Then,basedonbehaviorfinancetheory,weanalyzetheissuefrom4parts’behaviorandinterestinIPOactivitiesandfindoutwhyIPOunderpricinginChinaistoohigh.Fromtheanalysisanddiscussion,webelievethattherealreasonofhighIPOunderpricinginChinaisthehighpriceinexchangemarket.Ononehand,GovernmentcontrollingIPOleadstothelackofstocksandincreasethepriceinexchangemarket.Ontheotherhand,thegovernment’sdominantfunctioninIPOpricingkeepsthespreadbetweentheIPOmarketandtheexchangemarket.TheotherreasonthathighIPOunderpricingexistsinalongtimeisthattheIPOcompanieshavelittlepowertobargainintheIPOpricing.Atlast,wedrawaconclusionthathighIPOunderpricingisanequilibriuminpres

三七文档所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

三七文档所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

扫描二维码

扫描二维码

liuin916

liuin916

本文标题:中国股市IPO高抑价现象研究

链接地址:https://www.777doc.com/doc-6429441 .html