您好,欢迎访问三七文档

当前位置:首页 > 商业/管理/HR > 企业财务 > GlobalCFOStudy2008Summary[1]

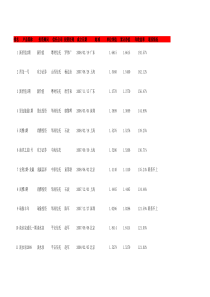

SummaryTheGlobalCFOStudy2008:BalancingRiskandPerformancewithinanIntegratedFinanceOrganizationTheGlobalCFOStudy2008:BalancingRiskandPerformancewithinanIntegratedFinanceOrganization,Rogers,Stephen,StephenLukens,SpencerLin,EdwinaJon.IBMGlobalBusinessServicesincooperationwiththeWhartonSchoolandEconomistIntelligenceUnit,64pages,2008.TopicalArea:CFO’sRoleinRiskManagement;IntegratedFinanceOrganization;RiskEventTrends;StateofRiskManagement;GlobalizationandRisks..MainTheme:ThisIBMstudyof1,200CFOsandseniorfinanceprofessionalsrevealsthatCFOsmaybetakingthewrongapproachtoresourceandriskmanagementonaglobalscale.Docurrentfinancialmanagementmodelshavesufficientflexibilitytoenableanenterprisetomakethestrategictransformationtoaglobalorganization?ThisstudyanalyzesthisissueandprovidesuniquedataaboutcurrentERMtrends.SummaryofReport:Two-thirdsoflargeenterprises(revenuesover$5billion)haveencounteredmaterialriskeventsinthelastthreeyears.Almosthalfofthosewerenotpreparedfortheevent.Onlyhalfofthesurveyparticipantshaveanyformalriskmanagementprogram.SurveyresultsindicatethatCFOshavetroubleprioritizingriskandrankedalmostallrisksequallyas“veryimportant.”Theyalsomaybemissingsomeimportantstrategicimperatives:TwoagendaitemsthattheCFOsrankedlowestinimportance–managing/mitigatingenterpriseriskanddrivingintegrationofinformationacrosstheenterprise–arekeydifferentiatorsforoutperformersinrevenueandstockpricegrowth.OverviewofStudyFindingsThisCFOsurveywasconductedbyIBM’sGlobalBusinessServicesdivision,incooperationwithTheWhartonSchoolandtheEconomistIntelligenceUnit.Theteamposed34questionstomorethan1,200CFOsandsenior-levelfinanceprofessionalsinfivemajorsectorsandacross79countries.Thepurposeofthesurveywastodeterminethestateofriskeventswithinorganizationssurroundingtheworld,andthestatusofcurrentmanagementprocessestoaddressriskevents.Keyfindingsincludethefollowing:•Sixty-twopercentofenterprisessurveyedwithrevenuesover$5billion(U.S.dollars)encounteredamaterialriskeventinthelastthreeyears.•Ofthose,42percentadmittedtonotbeingwellpreparedfortheevent.•Forty-sixpercentofenterprisessurveyedwithrevenuesunder$5billion(U.S.dollars)hadamajorriskeventand39percentwerenotwellprepared.•Risksarisefrommanyactivitiesbeyondfinancialrelatedriskdrivers.Eighty-fivepercentofrisktypesthatledtoacompany’smarketcapitalizationdeclineof30percentormorewerenon-financialinnature.•Themostfrequentlymentionedrisks(32percentofrespondents)relatedtostrategicrisks,whicharerisksrelatedtomarkets,customers,products,M&Aactivity,andotherbusinesstopics.•Geopoliticalandenvironmental/healthriskswerealsomoreprevalentthanfinancialrisks.•Onlyabout52percentofallsurveyedacknowledgedhavinganysortofformalizedriskmanagementprogram.•CFO’shavedifficultyprioritizingrisks–nearlyeveryfinanceactivityinthesurveywascategorizedas“veryimportant.”But,thereweregapsaswideas38percentregardinghoweffectivetheywereattacklingthoseactivities.•Only42percentofrespondentsdohistoriccomparisonstoavoidrisksandonly32percentsetspecifiedriskthresholds,withonly29percentcreatingrisk-adjustedforecastsandplans.•Thestudyidentifiedtwomajordifferentiatorsforfinancialoutperformance:-Increasedeffectivenessindrivingintegrationofinformationacrosstheenterprise-Increasedeffectivenessinsupporting,managing,andmitigatingenterpriseriskTheIntegratedFinanceOrganizationTheauthors’interviewsandstatisticalanalysesassistedtheminunderstandingwhatcharacteristicsinformationintegrationacrossanenterpriseshouldpossess.Theyconsiderthesecomponentspartofgoodgovernanceandwhattheycallthe,“IntegratedFinanceOrganization”or“IFO.”IFOshelptodriveintegrationofinformationacrosstheorganization.Analysisshowsthatcommondatadefinitions,astandardchartofaccounts,andstandardcommonpracticesenterprisewidearestronglycorrelatedtoincreasedeffectivenessatdrivingintegrationofinformation.Thus,globallymandatedstandardsforallfinanceoperationsacrosstheenterprisecanbeacriticalsuccessfactorsandIFOshelpprovidethatleadership.ThesurveyfindsthatenterpriseswithIFOshadrevenuegrowthratesnearlydoublethatoftheirindustrypeers.IFOsareoftenmorepreparedforriskbecausetheyaremoreawareofrisk,whichallowsthemtobemoreresponsivetoriskevents.IFOsself-reportthattheyare1.4timesmorelikelythannon-IFOstobeeffectiveatsupporting,managing,andmitigatingenterpriserisks.IFO’saretwiceaslikelytobepreparedformajorriskevents,andIFOsclaimtheyare1.3timesmoreawareofrisks.Thus,integrationofkeyfinancecomponentswithintheorganizationcreatessignificantstrategicadvantage.ProvidingtheTruthOutperformanceandriskmanagementareaboutgettingtothetruth.IFOsgetthetruthinaconsistentmannerasaresultoftheirenterprisestandardization.Theconsistentaccuracyofinformationhelpsmoveanorganizationfromtransactionaltoanalyticalhandlingofinformation-“taillightstoheadlights.”Incontrast,non-IFOsoftenfindthateverylayerandorganizationalsegmentrequiresalevelofinterpretationorreconciliationtoprovideaunifiedpointofview.Forthem,thelackofintegrationmakestheroll-upofinformationdifficultandoftenlessmeaningful.Twoactionsareessentialtoprovidingthetruth:establishingglobalstandar

三七文档所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

三七文档所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

扫描二维码

扫描二维码

d27661297

d27661297

本文标题:GlobalCFOStudy2008Summary[1]

链接地址:https://www.777doc.com/doc-1112998 .html